For most depositors, a bank failure raises one practical question: is my money safe? In nearly every case, the answer is yes — FDIC insurance protects deposits up to $250,000 per depositor per ownership category at each insured bank, and the resolution at Community Bank and Trust – West Georgia worked exactly the way the system is designed to work. But the closure is also a useful prompt to know how to check the financial health of any U.S. bank, because the publicly available data that signals trouble is more accessible than most consumers realize.

What happened at Community Bank and Trust – West Georgia

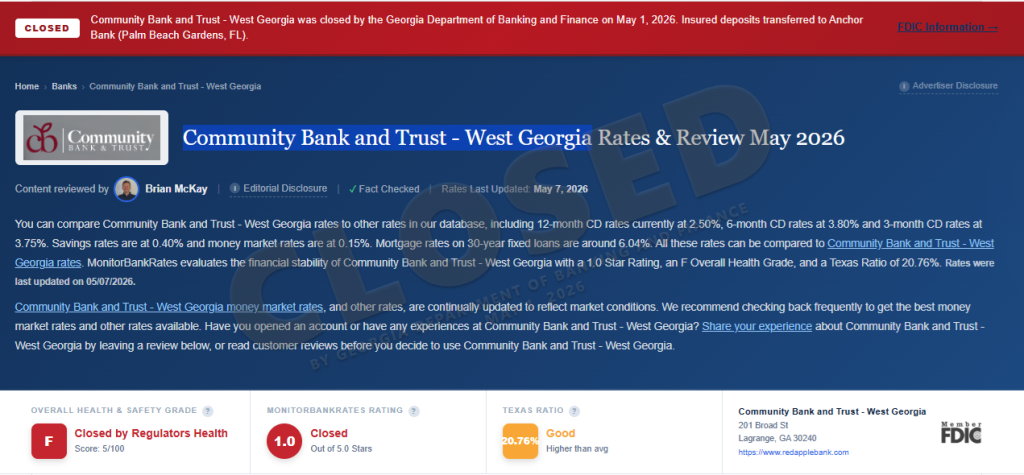

The bank, headquartered in LaGrange, Georgia, had $288 million in total assets and $268 million in total deposits as of December 31, 2025, operating three branches in west Georgia. Approximately $27 million of those deposits exceeded the $250,000 FDIC insurance limit at the time of the closure.

The closure followed a sequence of regulatory findings over the preceding four months. In January 2026, the Federal Reserve Bank of Atlanta conducted an inspection of Community Bankshares Inc., the bank’s holding company. According to the Federal Reserve’s subsequent disclosure, the inspection identified operational deficiencies “with respect to pursuit of its growth strategy, related to board oversight, capital, and compliance with the rules related to affiliate transactions.” In April 2026, the Federal Reserve issued a formal enforcement action against the holding company. Two weeks later, on May 1, the Georgia Department of Banking and Finance closed the bank.

The FDIC’s purchase-and-assumption transaction with Anchor Bank moved through over a single weekend. Insured deposit accounts transferred automatically. Customers continued using checks, debit cards, and direct deposits without interruption. Branches reopened Monday morning under Anchor Bank’s name. The full closure details remain available on the Community Bank and Trust – West Georgia profile page, which includes the bank’s last reported FDIC financial data and the closure timeline.

For the roughly $27 million in uninsured deposits, the picture is more complicated. Recovery on uninsured balances depends on the sale of the failed bank’s retained assets and is not guaranteed to be complete. The FDIC may issue advance dividends to uninsured depositors as asset sales progress, but the timeline and final recovery percentage will not be known for some time.

How to check whether your bank is financially healthy

The publicly available data that helps consumers evaluate bank safety is more straightforward than it appears. Three signals cover most of the value.

The Texas Ratio. This is the single most useful number consumers can look at. It compares a bank’s non-performing assets and loans 90 days past due to its tangible common equity plus loan loss reserves. The national average for U.S. banks is currently 5.85%. Ratios in line with or below that average indicate strong financial health. Ratios at two times the national average or higher warrant attention, even if the absolute number sits below traditional distress thresholds. Ratios above 100% are historically associated with serious distress. Every institution profile page on MonitorBankRates displays the Texas Ratio along with a comparison to the national average — searchable by bank or credit union name.

Recent regulatory enforcement actions. Federal Reserve, FDIC, and OCC enforcement actions are public record. They appear in the Federal Financial Institutions Examination Council’s National Information Center at ffiec.gov, searchable by institution name. An enforcement action against a bank or its holding company within the past 12 months is a meaningful signal — even when the bank’s headline financial numbers look fine. Enforcement actions are the closest thing to a real-time safety alert the regulatory system produces.

FDIC insurance coverage. This is the most important step and the one that genuinely makes the safety question secondary. If deposits at any single bank are within $250,000 per ownership category, FDIC insurance protects them regardless of the bank’s financial health. Joint accounts, retirement accounts, and trust accounts each carry separate $250,000 coverage at the same institution, which expands coverage substantially within one bank. Deposits above the limits should be spread across multiple FDIC-insured banks. The FDIC’s EDIE tool at edie.fdic.gov calculates insurance coverage for any account structure. For more on how FDIC insurance interacts with different account types and products, our guide on whether money market accounts are safe walks through the specific coverage rules.

What to do if you find something concerning

The first thing to remember is that FDIC insurance protects deposits within coverage limits regardless of the bank’s financial state. The Community Bank and Trust – West Georgia closure followed the FDIC’s preferred resolution path: insured depositors regained access to their funds within hours, branches reopened the next business day, and customers continued banking without disruption. The $97 million cost of the failure is borne by the FDIC’s Deposit Insurance Fund, which is funded by premiums paid by FDIC-insured banks — not by taxpayers, and not by depositors at the failed institution.

For deposits above insurance limits, the response is straightforward: spread balances across institutions before any problem develops. Each separate FDIC-insured bank carries its own $250,000 per-ownership-category coverage. A depositor with $750,000 in cash can fully insure that money by holding $250,000 at three different banks. Adding a joint owner, opening a trust account, or holding retirement funds at the same institution can also expand effective coverage at a single bank.

For depositors who simply want to be in a stronger institution, comparing your current bank’s numbers against the broader market is straightforward. MonitorBankRates tracks 8,500+ banks and credit unions across all 50 states with current rates and full financial profiles for each, including Texas Ratio, capitalization, and safety grade. Moving deposits to a higher-rated institution that also pays a competitive rate is often a meaningful upgrade on both safety and yield. Compare current rates across product categories: CD rates, savings rates, money market rates, and checking account rates.

Why we’re seeing more failures right now

Two failures in the first four months of 2026 is a faster pace than 2025, which saw two failures the entire year (Pulaski Savings Bank in January and Santa Anna National Bank of Texas in June), but well below the 2008–2010 cycle that averaged more than 100 failures per year. The 2023 cycle that included Silicon Valley Bank and First Republic involved larger institutions but fewer total failures.

The 2026 failures so far have been smaller community banks with operational and supervisory issues at the holding company level — Metropolitan Capital Bank & Trust of Chicago in January and Community Bank and Trust – West Georgia in May, both under $300 million in assets. For depositors at large national banks with diversified loan portfolios and strong capital ratios, the risk environment looks similar to any normal year. For depositors at smaller community banks with concentrated loan portfolios or recent regulatory findings, knowing how to combine quarterly data with real-time signals matters more.

For ongoing context on how Federal Reserve policy interacts with deposit and lending rates more broadly, our analysis of what the Fed’s recent rate hold means for CD rates through 2026 walks through the broader rate environment, and our housing affordability index report tracks how rate movement affects mortgage borrowers in real time.

Frequently Asked Questions

Are my deposits at risk if my bank fails?

Not if they are within FDIC insurance limits. The FDIC insures deposits up to $250,000 per depositor, per insured bank, for each account ownership category. Credit union deposits carry equivalent protection through the NCUA. Joint accounts, trust accounts, and retirement accounts each carry separate coverage at the same institution. Deposits above the limits are partially recovered through the sale of the failed bank’s assets but are not guaranteed to be made whole.

What is the Texas Ratio and what’s a safe number?

The Texas Ratio compares a bank’s non-performing assets and loans 90 days past due to its tangible common equity plus loan loss reserves. The national average for U.S. banks is currently 5.85%. Ratios at or below the national average indicate strong financial health. Ratios at two times the national average or higher warrant attention. Ratios above 100% have historically been associated with serious distress.

How quickly does FDIC insurance pay out after a failure?

In most cases, depositors regain access to insured funds within one to two business days. The FDIC’s preferred resolution method is a same-weekend purchase-and-assumption transaction, in which another FDIC-insured bank acquires the failed bank’s deposits and reopens its branches under new ownership the next business day. The Community Bank and Trust – West Georgia resolution followed this pattern: closed Friday May 1, branches reopened as Anchor Bank Monday May 4.

Should I worry about deposits over $250,000?

If deposits at a single bank exceed $250,000 in a single ownership category, the excess is uninsured. The simplest fix is to spread deposits across institutions. Joint accounts, retirement accounts, and trust accounts each carry separate $250,000 coverage at the same bank, which can substantially expand insured totals within one institution. The FDIC’s EDIE tool at edie.fdic.gov calculates exact coverage for any account structure in about two minutes.

How can I check whether my bank has any regulatory enforcement actions?

The Federal Financial Institutions Examination Council maintains the National Information Center at ffiec.gov, where Federal Reserve, FDIC, and OCC enforcement actions are searchable by institution. Holding company actions are sometimes filed separately from bank-level actions, so it’s worth searching for both. Recent enforcement actions carry more weight than older ones, since underlying issues may have been addressed over time.

Where can I find a full list of failed banks?

The FDIC maintains a complete list of failed banks at fdic.gov/bank-failures. The list dates back to 1934 and includes details on each closure, the assuming institution if any, and the cost to the Deposit Insurance Fund. Community Bank and Trust – West Georgia is the second 2026 failure on that list, following Metropolitan Capital Bank & Trust of Chicago in January.